Impact of UIFW Functioning on Municipalities in South Africa

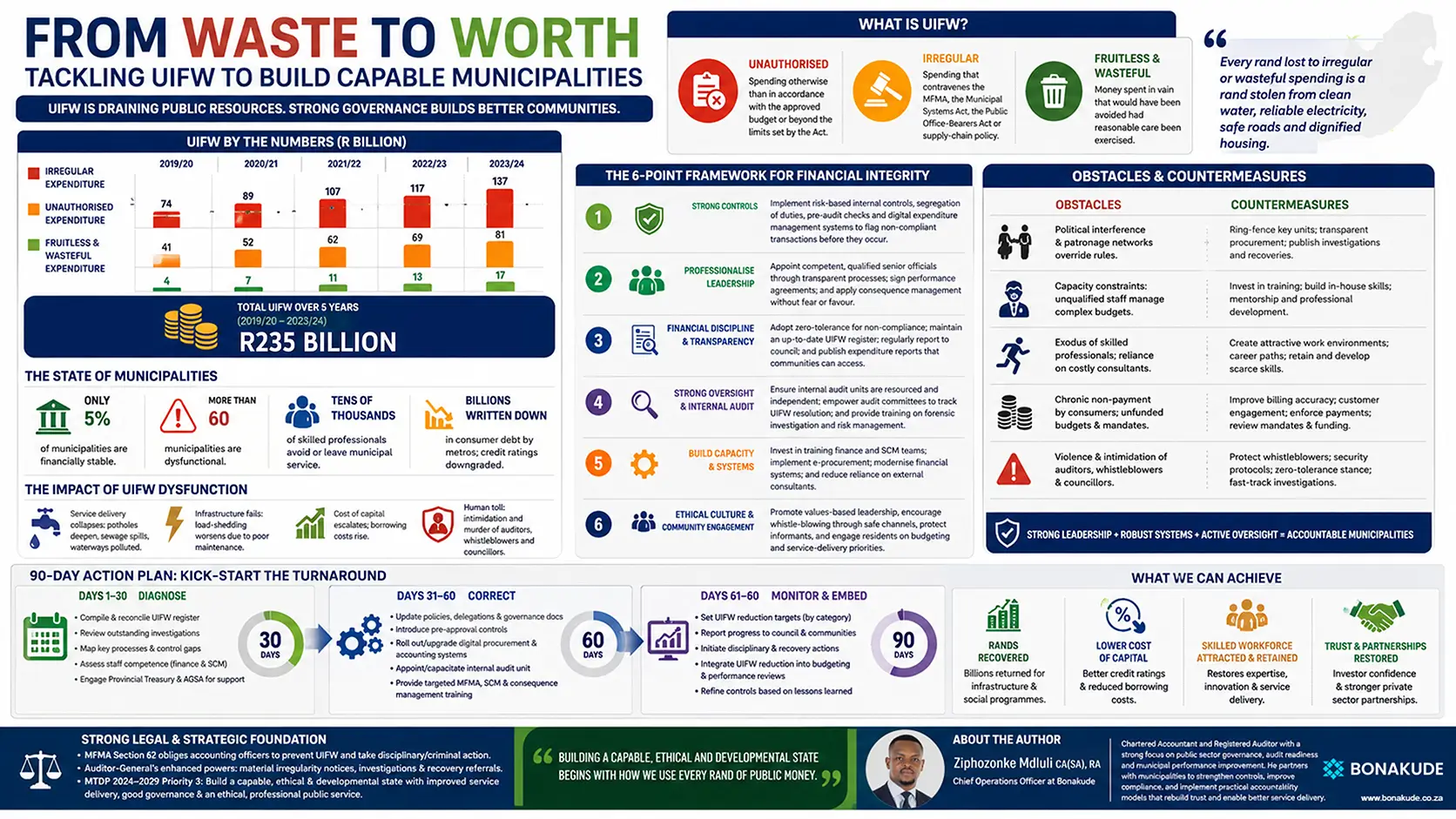

Unauthorised, irregular, fruitless and wasteful (UIFW) expenditure has evolved from an accounting anomaly to a systemic crisis. Between the 2019/20 and 2023/24 financial years, municipalities and municipal entities collectively reported more than R1.08 trillion in UIFW expenditure, with irregular expenditure alone rising from R74 billion to R137 billion over five years. Unauthorised expenditure spiked from R41 billion to R81 billion, while fruitless and wasteful expenditure increased from R4billion to R17 billion.

Author: Ziphozonke Mdluli CA(SA), RA – Chief Operations Officer at Bonakude

What Is UIFW Expenditure in South African Municipalities?

The Auditor-General notes that such spending undermines compliance with the Municipal Finance Management Act (MFMA) and diverts resources from essential services to investigations, condonement processes and litigation.

Only about five percent of municipalities are deemed financially stable, with more than sixty described as dysfunctional due to weak governance, poor institutional capacity and political interference. These failures have tangible consequences. Service delivery collapses as potholes deepen, sewage spills contaminate waterways and load-shedding worsens because municipalities cannot maintain electricity infrastructure.

The cost of capital escalates as rating agencies downgrade metros that have written down billions in consumer debt and failed to produce funded budgets. The human toll is devastating: whistleblowers, auditors and councillors have been intimidated and murdered, and tens of thousands of skilled professionals avoid or leave municipal service.

This dysfunction contradicts the Medium-Term Development Plan (MTDP) 2024–2029’s third strategic priority – to build a capable, ethical and developmental state with improved service delivery, good governance and an ethical, professional public service.

The Legal Duties of Municipal Accounting Officers

The MFMA and the Municipal Systems Act establish clear definitions and duties regarding UIFW. Irregular expenditure refers to spending that contravenes the MFMA, the Municipal Systems Act, the Public Office-Bearers Act or the municipality’s supply-chain management policy. Unauthorised expenditure is any spending otherwise than in accordance with the approved budget or beyond the limits set by the Act. Fruitless and wasteful expenditure is money spent in vain that would have been avoided had reasonable care been exercised.

Section 62 of the MFMA obliges accounting officers to prevent such expenditures and to pursue disciplinary or criminal action against officials who commit financial misconduct. The Auditor-General’s enhanced powers under the amended Public Audit Act enable her office to issue material irregularity notices and refer matters for investigation and recovery.

The MTDP emphasises that building a capable, ethical state requires improved service delivery in local government, improved governance and performance of public entities, and an ethical and professional public service. This strategic priority underscores the urgency of tackling UIFW and asks: how can municipalities deliver the infrastructure and services envisioned by the National Development Plan if they cannot first halt the bleeding of public funds?

A Six-Point Framework for Reducing UIFW

Responding to UIFW requires more than compliance checklists. It demands a framework that institutionalises accountability, professionalism and transparency. The following six principles offer a blueprint for municipalities seeking to restore financial integrity and public trust:

- Establish strong preventative and detective controls: implement risk-based internal controls, segregation of duties, pre-audit checks and digital expenditure management systems to flag non-compliant transactions before they occur.

- Professionalise leadership and enforce accountability: appoint competent, qualified senior officials through transparent processes; sign performance agreements; and apply consequence management without fear or favour when legislation is breached.

- Embed financial discipline and transparency: adopt a zero-tolerance stance toward non-compliance; maintain an up-to-date UIFW register; regularly report to council; and publish expenditure reports that communities can access.

- Strengthen internal audit and oversight functions: ensure internal audit units are adequately resourced and independent; empower audit committees to track UIFW resolution; and provide training on forensic investigation and risk management.

- Build organisational capacity and systems: invest in training procurement and finance teams; roll out e-procurement platforms to reduce manual processes; modernise financial systems; and reduce reliance on external consultants by developing in-house skills.

- Cultivate an ethical culture and engage communities: promote values-based leadership, encourage whistle-blowing through safe reporting channels, protect informants, and engage residents on budgeting and service-delivery priorities to rebuild social trust.

Click the infographic to enlarge.

Strengthening Controls, Oversight and Consequence Management

Municipalities face formidable obstacles in addressing UIFW. Political interference and patronage networks often override procurement rules, discouraging officials from challenging irregularities. Capacity constraints result in unqualified staff managing complex budgets, while the exodus of skilled professionals leaves municipalities reliant on expensive consultants whose work is sometimes ineffective. Chronic non-payment by consumers undermines revenue streams, creating unfunded budgets and unfunded mandates. Violence and intimidation against auditors and whistleblowers foster a culture of fear and silence.

To counter these challenges, councils must ring-fence internal audit and supply-chain units from political influence and allocate sufficient resources for training and systems. Protective mechanisms for whistleblowers and audit staff should be institutionalised, drawing on the MTDP’s call for an ethical and professional public service. National Treasury and provincial treasuries can deploy support teams to stabilise finances in distressed municipalities and vet procurement above set thresholds.

A culture of accountability can be strengthened through performance contracts, rotation of supply-chain roles, and the publication of UIFW investigations and recoveries. Municipalities should also improve revenue management by adopting accurate billing, customer engagement, and enforcement to ensure service users pay for services rendered.

A 90-Day UIFW Turnaround Plan for Municipalities

A phased approach over 90 days can kick-start the turnaround journey and demonstrate tangible progress:

- Days 1–30: Conduct a comprehensive diagnostic. Compile and reconcile the UIFW register; review outstanding investigations; map key processes; assess the competence of finance and supply-chain staff; and consult provincial treasury and the Auditor-General’s office for support.

- Days 31–60: Implement corrective measures. Update policies and delegations; introduce pre-approval controls; roll out or upgrade digital procurement and accounting systems; appoint or capacitate an internal audit unit; and provide targeted training on the MFMA, supply-chain management and consequence management.

- Days 61–90: Monitor, report and embed. Set clear reduction targets for each category of UIFW; report progress to council and communities; initiate disciplinary or recovery processes where wrongdoing is confirmed; integrate UIFW reduction into budgeting and performance reviews; and refine controls based on lessons learned.

Why Tackling UIFW Supports the MTDP 2024–2029

Addressing UIFW is not merely a compliance exercise; it is a moral and economic imperative. Every rand lost to irregular or wasteful spending is a rand stolen from clean water, reliable electricity, safe roads and dignified housing.

Eliminating UIFW can free billions of rands for investment in infrastructure and social programmes, reduce borrowing costs and improve municipal credit ratings. An ethical culture and competent leadership will attract and retain scarce skills, restore investor confidence and unlock partnerships with the private sector.

Ultimately, delivering on the MTDP’s vision of a capable, ethical and developmental state depends on municipalities demonstrating that public funds are used effectively, efficiently and in the public interest.

Author Bio

Ziphozonke Mdluli CA(SA), RA is a Director and Chief Operations Officer at Bonakude with more than 24 years auditing experience in the public and private sectors.

He is a seasoned Chartered Accountant and Registered Auditor. Over the years, he has conducted several audits in the Public Sector, servicing Municipalities, National and Provincial Government Departments, Higher Education & Training Entities, and Public Entities. In the Private Sector, he has serviced entities in Healthcare, Mining, and Engineering industries.

His key areas of expertise include: Combined Assurance; Risk Management; AFS Review and Audit; Forensic Audit and Investigations; Probity Audits; and Regularity Audits.

Frequently Asked Questions

What does UIFW expenditure mean?

UIFW stands for unauthorised, irregular, fruitless and wasteful expenditure. It refers to public money that has been spent outside approved budgets, in breach of legislation or policies, or in a way that delivers no value because reasonable care was not taken.

Why is UIFW a problem for municipalities?

UIFW weakens financial management, diverts resources away from essential services and damages public trust. It also increases the burden on councils, audit committees and officials who must investigate, report and resolve the expenditure.

How much UIFW expenditure have South African municipalities reported?

Between the 2019/20 and 2023/24 financial years, municipalities and municipal entities collectively reported more than R1.08 trillion in UIFW expenditure.

What causes UIFW expenditure?

Common causes include weak internal controls, poor procurement practices, political interference, lack of consequence management, capacity constraints, poor oversight and inadequate financial systems.

How does UIFW affect service delivery?

When public funds are lost to irregular or wasteful spending, municipalities have fewer resources for water, sanitation, roads, electricity, housing and infrastructure maintenance. This contributes to service delivery failures and declining community trust.

What is irregular expenditure?

Irregular expenditure is spending that contravenes legislation such as the Municipal Finance Management Act, the Municipal Systems Act, the Public Office-Bearers Act or a municipality’s supply-chain management policy.

What is unauthorised expenditure?

Unauthorised expenditure is spending that is not in line with the approved municipal budget or that exceeds limits set by law.

What is fruitless and wasteful expenditure?

Fruitless and wasteful expenditure is spending made in vain that could have been avoided if reasonable care had been exercised.

How can municipalities reduce UIFW?

Municipalities can reduce UIFW by strengthening controls, maintaining accurate UIFW registers, improving procurement processes, professionalising leadership, empowering internal audit, enforcing consequence management and reporting transparently to council and communities.

How can Bonakude support municipalities?

Bonakude supports municipalities and public institutions by strengthening governance, improving audit readiness, supporting compliance, building accountability models and helping leadership teams implement practical systems that improve financial management and service delivery.