Municipal Asset Management in South Africa:

Protecting Service Delivery, Revenue and Clean Audit Outcomes

“Municipal assets form the foundation of service delivery in South Africa’s local government system. Roads, water infrastructure, electricity networks, wastewater treatment works, public buildings, fleet, plant and equipment, heritage assets and information systems are the platforms through which municipalities deliver basic services, enable local economic activity, protect public health and build trust with communities.”

Author: Prosper Mutambirwa AGA (SA) – Senior Manager: Consulting at Bonakude

The Strategic Foundation of Service Delivery and Financial Sustainability

When municipal assets are properly planned, recorded, maintained and monitored, they support reliable service delivery and improve municipal financial sustainability. When they are poorly managed, the consequences are visible in water interruptions, electricity distribution losses, failing roads, sewer spillages, weak billing, audit qualifications and rising community frustration.

This makes municipal asset management a strategic governance issue; being not only a technical function for finance teams or engineers, but a cross-functional responsibility that links the municipal manager, chief financial officer, technical services, infrastructure planning, internal audit, revenue management, council oversight and community accountability.

Why Municipal Asset Management Matters Now

South Africa’s local government environment is under intense pressure with municipalities expected to deliver more reliable services, improve audit outcomes, strengthen revenue collection and maintain ageing infrastructure, often within constrained budgets and limited technical capacity.

The latest municipal audit and performance reports point to a clear reality; infrastructure condition, financial sustainability and accountability are inseparable. Municipalities cannot achieve sustainable clean audits while asset registers are unreliable, maintenance plans are weak, infrastructure projects are poorly monitored, and service delivery assets are not linked to revenue protection.

The Auditor-General’s recent local government reporting continues to show that too few municipalities achieve clean audits, while many face financial strain, unfunded budgets, poor record-keeping, weak project management and recurring non-compliance. At the same time, water and electricity losses continue to erode revenue. In practical terms, municipalities are losing income from services they have already paid to produce, treat, purchase or distribute.

Water infrastructure is a particularly urgent example with national regulatory reporting showing that non-revenue water has increased significantly over the past decade. This includes physical losses through leaks, commercial losses through illegal connections or metering gaps, and administrative losses linked to weak billing and revenue systems. Wastewater infrastructure also presents material service delivery, environmental and public health risks where treatment works are poorly maintained or underperforming.

The message for municipal leaders is direct: asset management is no longer a back-office compliance exercise. It is a frontline service delivery discipline.

The Legal and Governance Foundation

The Municipal Finance Management Act places responsibility on the accounting officer to manage, safeguard and maintain municipal assets and liabilities. This includes ensuring that the municipality has appropriate systems to account for assets, value them in line with recognised accounting practice, maintain internal controls, and keep an asset and liabilities register.

In practice, this means every municipality should be able to answer five basic questions with credible evidence:

- What assets do we own or control?

- Where are those assets located?

- What condition are they in?

- What value and useful life remain?

- What maintenance, renewal or replacement decisions are required?

If a municipality cannot answer these questions confidently, it will struggle to produce reliable annual financial statements, prepare credible maintenance budgets, defend audit evidence, prioritise infrastructure investment or explain service delivery failures to communities.

A compliant asset register is therefore only the starting point. The real objective is an integrated asset management system that connects financial records, technical condition assessments, GIS location data, maintenance plans, depreciation, impairment, insurance, capital projects, revenue streams and service delivery risk.

Asset Registers Must Move Beyond Spreadsheets

Many municipalities still experience asset management problems because asset registers are treated as year-end audit files rather than live management tools. This creates several recurring weaknesses:

- Assets recorded in the financial system do not always reconcile to assets physically verified on site.

- Infrastructure condition assessments are outdated or incomplete.

- Capital work-in-progress is not transferred timeously to completed assets.

- Repairs and maintenance are incorrectly classified as capital expenditure, or capital expenditure is incorrectly treated as operating expenditure.

- Useful lives, residual values, impairment indicators and depreciation assumptions are not reviewed consistently.

- Asset records are not linked to maintenance schedules, service interruptions or revenue losses.

A modern municipal asset register should be digital, centralised, regularly updated and supported by verifiable evidence. It should include photographs, GPS coordinates, componentisation of major infrastructure, condition ratings, maintenance history, valuation records and clear ownership of updates.

For public infrastructure, this level of detail is essential. A water treatment plant, road network, electricity substation or municipal building is not a single static item, but is a service delivery system made up of components that age, fail, require maintenance and affect communities differently.

The Link Between Assets, Revenue and Performance

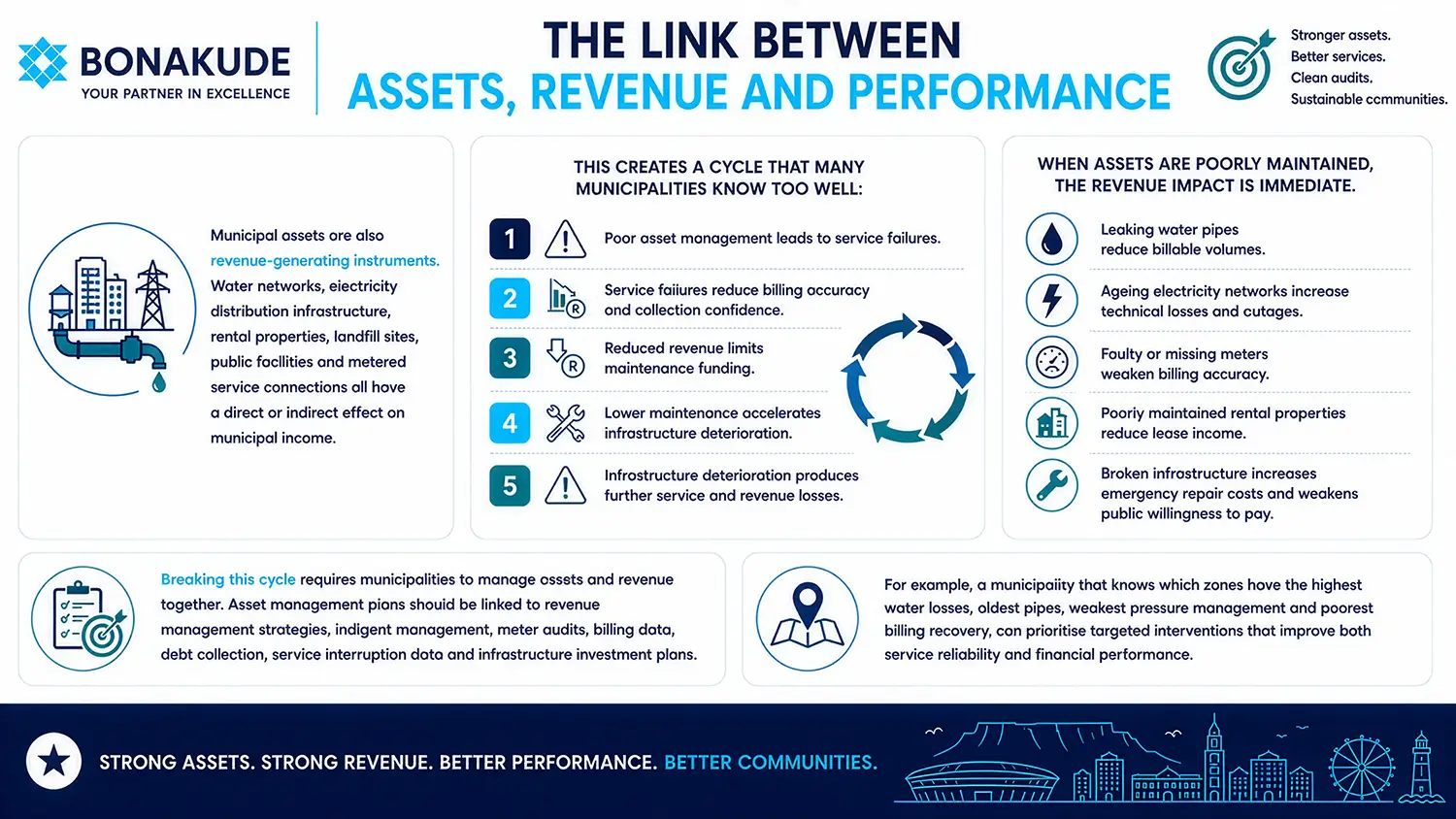

Municipal assets are also revenue-generating instruments. Water networks, electricity distribution infrastructure, rental properties, landfill sites, public facilities and metered service connections all have a direct or indirect effect on municipal income.

When assets are poorly maintained, the revenue impact is immediate. Leaking water pipes reduce billable volumes. Ageing electricity networks increase technical losses and outages. Faulty or missing meters weaken billing accuracy. Poorly maintained rental properties reduce lease income. Broken infrastructure increases emergency repair costs and weakens public willingness to pay.

This creates a cycle that many municipalities know too well:

- Poor asset management leads to service failures.

- Service failures reduce billing accuracy and collection confidence.

- Reduced revenue limits maintenance funding.

- Lower maintenance accelerates infrastructure deterioration.

- Infrastructure deterioration produces further service and revenue losses.

Breaking this cycle requires municipalities to manage assets and revenue together. Asset management plans should be linked to revenue management strategies, indigent management, meter audits, billing data, debt collection, service interruption data and infrastructure investment plans.

For example, a municipality that knows which zones have the highest water losses, oldest pipes, weakest pressure management and poorest billing recovery, can prioritise targeted interventions that improve both service reliability and financial performance.

Audit Outcomes and the Asset Management Challenge

The Auditor-General’s municipal audit outcomes continue to show that poor record-keeping, weak internal controls, incomplete evidence and unreliable financial reporting undermine accountability. Asset management is often central to these challenges.

A municipality may receive audit findings where it cannot provide sufficient evidence for the existence, completeness, valuation, depreciation, impairment or ownership of assets. It may also face findings where repairs and maintenance expenditure is not properly classified, capital projects are not recorded correctly, or infrastructure assets are not supported by adequate documentation.

Clean audit outcomes require a control environment where asset information is captured correctly at source, updated throughout the year, reviewed by management, reconciled to the general ledger, and supported by internal audit oversight. These are not simply technical year-end adjustments.

This means asset management must be embedded into monthly and quarterly reporting, not left for annual financial statement preparation. A strong municipality should know its asset risks before the audit, not discover them through audit findings.

Repair or Build New? The Answer Is Lifecycle Management

Municipal leaders are often faced with a difficult decision: should the municipality repair existing infrastructure or build new infrastructure?

The answer is not binary. It depends on condition, capacity, demand, cost, risk and long-term sustainability.

Repair and refurbishment should be prioritised where existing infrastructure can still deliver the required service level at a reasonable lifecycle cost. Preventive maintenance is usually more cost-effective than emergency replacement, and it reduces service disruptions. In a constrained fiscal environment, extending the useful life of viable assets is often the most responsible decision.

However, new infrastructure becomes necessary where demand exceeds capacity, where assets are beyond economical repair, where technology has become obsolete, or where growth requires expanded service networks. Municipalities with growing populations, expanding informal settlements, industrial development corridors or new housing projects cannot rely only on ageing infrastructure.

The correct approach is lifecycle asset management. This means each asset should be assessed across its full lifecycle: planning, acquisition, construction, operation, maintenance, renewal, disposal and replacement. Decisions should be based on evidence, not only on short-term political pressure or the availability of grant funding.

The Way Forward for Municipalities - 7 Practical Steps

South African municipalities require a hybrid asset management strategy that prioritises maintenance and refurbishment where assets can be salvaged, while enabling strategic new investment where demand and risk justify it. The following actions provide a practical framework.

1. Establish Centralised, Digital Asset Registers

A centralised, digital asset register is the foundation of transparency and accountability. It should consolidate municipal assets into one reliable platform and link financial records to physical verification, technical condition, location, ownership and maintenance history.

This improves audit readiness, supports better budgeting, reduces duplication, limits the risk of ghost assets, and gives management a clearer view of service delivery risks.

A strong digital register should include:

- Asset description and classification

- Location and GPS coordinates

- Cost, valuation and accumulated depreciation

- Useful life, residual value and impairment indicators

- Condition assessment and criticality rating

- Custodian department

- Maintenance history

- Supporting evidence such as photographs, invoices, title deeds, completion certificates and project close-out documentation

2. Implement Lifecycle Asset Management Standards

Municipalities should manage assets as systems with predictable lifecycle stages. This requires maintenance plans, renewal schedules, condition assessments and replacement strategies that are aligned to the Integrated Development Plan, Service Delivery and Budget Implementation Plan and long-term financial plan.

Lifecycle planning helps municipalities move from reactive maintenance to preventive maintenance. Instead of waiting for a pump station to fail, a road to collapse or a transformer to burn out, the municipality can schedule inspections, servicing, refurbishment and renewal before failure disrupts communities.

This approach reduces emergency procurement, lowers long-term costs, extends asset life and improves service continuity.

3. Link Asset Management to Revenue Protection

Municipal asset management should not operate separately from revenue management. Water, electricity and property-related assets should be linked to billing, metering, consumption, losses, debtor management and collection strategies.

Municipalities should identify which infrastructure assets contribute most directly to revenue and which assets present the highest financial leakage risk. This can include water distribution networks, reservoirs, pump stations, electricity substations, transformers, meters, rental properties and landfill operations.

A practical revenue-linked asset plan should include:

- Meter audits and meter replacement programmes

- Water loss and electricity loss analysis by zone

- Illegal connection and tampering risk assessments

- Maintenance plans for revenue-critical infrastructure

- Alignment between engineering data and billing data

- Debtor and indigent data cleansing

- Monthly reporting on service losses and revenue impact

When municipalities understand how asset condition affects income, maintenance becomes an investment in financial sustainability rather than a discretionary expense.

4. Strengthen Project and Grant Governance

Infrastructure grants are essential for addressing backlogs and expanding services, but grant spending only creates value when projects are planned, procured, delivered and capitalised correctly.

Municipalities should strengthen controls over capital projects by ensuring that every project has a clear business case, approved budget, implementation plan, contract management process, progress reporting, quality assurance, completion certificate and asset capitalisation process.

Weak project governance creates several risks. Projects may be delayed, funds may be underspent, work may be completed without proper quality controls, or assets may not be transferred correctly into the asset register. In some cases, municipalities spend money but do not receive the expected service delivery benefit.

A disciplined project governance model should connect infrastructure planning, supply chain management, technical oversight, finance, asset management and internal audit.

5. Build Technical Capacity Through Training and Partnerships

Many municipalities struggle with asset management because the required skills sit across finance, engineering, planning, ICT and audit. Smaller and rural municipalities often face shortages of engineers, asset accountants, data specialists and experienced project managers.

Capacity building should therefore be practical and sustained. Municipalities need structured training, standard operating procedures, skills transfer from consultants, partnerships with professional bodies, and clearer accountability for asset custodians.

Where consultants are used, the objective should not be dependency. The objective should be delivery with transfer of skills, improvement of systems and strengthening of internal capability.

6. Use Internal Audit and Oversight Structures More Effectively

Internal audit, audit committees, municipal public accounts committees and council oversight structures should play a stronger role in asset management. They should not wait for the external audit process to reveal weaknesses.

Internal audit plans should include asset verification, maintenance planning, capital project controls, revenue-linked infrastructure risks, grant spending, fleet management, ICT assets and asset disposal. Audit committees should request evidence that management has addressed recurring asset-related findings before year-end.

Effective oversight should ask:

- Are asset registers updated monthly or only at year-end?

- Are condition assessments current?

- Is the repairs and maintenance budget aligned to asset risk?

- Are capital projects capitalised timeously?

- Are water and electricity losses quantified and acted on?

- Are asset-related audit findings resolved permanently?

- Is there consequence management for negligence, poor record-keeping or non-compliance?

7. Engage Communities in Asset Decisions

Community engagement is often overlooked in asset management, yet communities experience the consequences of failing infrastructure first. Residents know where water leaks persist, which roads are unsafe, where streetlights are not working, and which facilities are deteriorating.

Municipalities should use ward committees, public consultations, IDP engagements and participatory budgeting to test asset priorities against community needs. This helps prevent misalignment between what municipalities build and what communities need most urgently.

A municipality may find that communities prefer the refurbishment of water infrastructure, sewer systems or roads over a new administrative building. This does not remove the need for technical assessment, but it strengthens legitimacy and improves trust.

The First 90 Days: A Municipal Asset Management Reset

Municipalities that want to strengthen asset management can begin with a focused 90-day reset plan:

Days 1–30: Diagnose

Review the fixed asset register, general ledger reconciliation, prior-year audit findings, capital work-in-progress, maintenance budgets, infrastructure condition reports and water/electricity loss data.

Days 31–60: Prioritise

Rank assets by service delivery criticality, revenue impact, condition and audit risk. Identify the assets most likely to cause service disruptions, revenue losses or audit qualifications.

Days 61–90: Act

Update the asset register, resolve evidence gaps, prepare a maintenance intervention plan, correct classification errors, assign asset custodians, and establish monthly asset management reporting to management and council oversight structures.

This approach creates momentum. It also gives municipal leaders a practical basis for budget adjustments, audit preparation, grant planning and service delivery improvement.

Bonakude’s Perspective

At Bonakude, we believe municipal asset management should be practical, evidence-based and linked to measurable public value. Strong asset management supports clean administration, better financial reporting, improved revenue, reduced infrastructure failure and stronger community confidence.

Our work across fixed asset registers, infrastructure verification, maintenance planning, revenue management, audit readiness, internal audit and public sector consulting has shown that municipalities can make meaningful improvements when technical teams, finance teams and leadership work from a shared evidence base.

The municipalities that will improve are not necessarily those with the largest budgets. They are the municipalities that know what they own, understand the condition of their infrastructure, maintain credible records, act on risks early, and make decisions based on lifecycle value.

Conclusion

Municipal assets are not passive financial records; they are the operating backbone of local government and the infrastructure through which communities experience the credibility, reliability and impact of public service delivery.

South Africa’s municipalities cannot afford to treat asset management as a once-a-year compliance exercise. The cost of weak asset management is too high; unreliable services, avoidable losses, audit findings, emergency repairs, poor community trust and declining financial sustainability.

The way forward is a hybrid, lifecycle-based asset management model. Municipalities must maintain and refurbish assets where it is cost-effective to do so, invest in new infrastructure where demand requires it, and build digital systems that connect assets to performance, revenue and accountability.

For municipal leaders, the question is no longer whether asset management matters. The question is whether their asset management systems are strong enough to protect service delivery, public money, and the communities they serve

Author Bio

Prosper Mutambirwa AGA (SA) has more than 15 years Auditing and Consulting experience in the Public and Private Sectors. He is a Senior Manager in the Consulting Division at Bonakude.

Throughout the years, Prosper has been involved in several auditing and consulting assignments in the Public Sector, servicing Municipalities, National and Provincial Government Departments, Higher Education & Training Entities, and Public Entities. In the Private Sector, he has serviced entities in Healthcare, Mining, and Engineering industries.

Prosper currently manages a portfolio with FAR assignments, that feed into the AFS Preparation.

His key areas of expertise include: Internal Audit; External Audit; Accounting; AFS & Audit Turnaround; Management Consulting; Fixed Asset Management; and Revenue Management.

Frequently Asked Questions

What is municipal asset management in South Africa?

Municipal asset management is the planning, recording, safeguarding, maintenance and renewal of assets used to deliver local government services.

Why is municipal asset management important for service delivery?

Reliable assets support water, electricity, roads, sanitation, public facilities and other services that communities depend on every day.

How does asset management support clean audit outcomes?

Strong asset records, reconciliations, evidence, valuations and controls help municipalities produce credible financial statements and reduce audit findings.

What should a municipal asset register include?

A strong register should include asset descriptions, locations, values, useful lives, condition ratings, custodians, maintenance history and supporting evidence.

How are municipal assets linked to revenue protection?

Water, electricity, property and metering assets affect billing, consumption, losses, collection confidence and the municipality’s ability to fund maintenance.

Should municipalities repair existing infrastructure or build new infrastructure?

The decision should be based on lifecycle evidence, including condition, capacity, demand, cost, risk and long-term sustainability.

What is a practical 90-day asset management reset?

A 90-day reset reviews asset records and risks, prioritises critical assets, closes evidence gaps and establishes monthly asset management reporting.

How can Bonakude support municipal asset management?

Bonakude supports municipalities with fixed asset registers, infrastructure verification, audit readiness, internal audit, revenue management and public sector consulting.